Property Tax Resources

How To Contest Clawbacks Provisions

"Companies out of compliance on tax abatement agreements can still make a compelling case for relief."

The race among states and cities to lure new companies and retain existing businesses has been furious, featuring aggressive offerings of significant tax allowances in exchange for promises of jobs and capital investment.

But taxpayers must be cautious. When the government lends a bigger hand that hand can claw back realized tax savings.

Deals involving property tax abatement usually include a promise by a business to invest certain sums of money in its properties and create and/or retain a certain number of jobs.

In return, the local taxing authority exempts all or a portion of the property taxes a business otherwise would have to pay on the new development over some specific period of time.

Governments often insist that abatement contracts permit them to recoup tax savings if a company falls short of its investment and/or hiring aims. Generally referred to as "clawbacks," these provisions in tax abatement agreements are becoming more commonplace and governments are keen on enforcing them.

Many current beneficiaries of tax abatements operate under agreements that originated prior to the recession that began in December 2007, when business expansion appeared more attainable.

However, new economic challenges have frustrated expansion objectives. And with governments mired in search of additional revenue, the potential for clawback appears greater.

Recognizing that clawback is a risk commensurate with the tax benefit, tax abatement recipients facing the prospect of clawback still have the possibility of avoiding the risk.

Escaping clawbacks

When a company enters into an abatement agreement with a municipality, it should be fully aware of the ramifications if the investment and/or hiring fall short of promised levels.

Agreements often allow taxing authorities to cancel abatements when companies fall out of compliance and may also require reimbursement of past tax savings in proportion to investment or employment shortfalls.

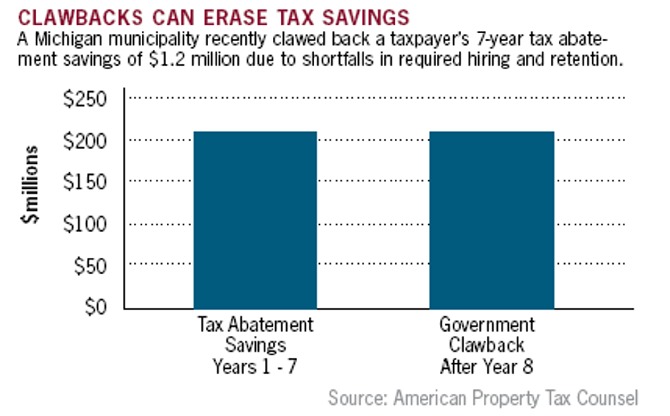

In other cases, noncompliance could mean recoupment by the tax collector of all tax abatement savings to date. Total recoupment of tax savings is illustrated in the chart above, where the recipient of a long-term abatement complied with job requirements for seven years but fell out of compliance in year eight, violating the abatement agreement.

When a clawback provision exists, the owner should examine the language to see if it applies to the circumstances of his property. Some clawback language might excuse shortcomings because of factors beyond the property owner's control.

This amorphous test often is tied to an unforeseeable reduction in demand for the company's product or services, or something similar. Because of the recent economic downturn, much litigation can be expected regarding these issues.

In some situations, a taxpayer should consider renegotiating the abatement agreement. A business can be in a surprisingly strong negotiating position, especially in instances where it can boast contributions to the local economy.

In some situations, a taxpayer should consider renegotiating the abatement agreement. A business can be in a surprisingly strong negotiating position, especially in instances where it can boast contributions to the local economy.

Confronted with the possibility of losing such a business to another municipality, local officials might be willing to work out a deal.

Where negotiation fails, a business can consider fighting the government's clawback.

Special attention should be paid to the applicable statutes. The local government's clawback effort might run afoul of statutory abatement cancellation and reimbursement schemes to such a degree that the provision should be nullified.

When a business has complied with abatement terms before the shortfall, a court might hesitate to award the government a windfall recoupment of all tax abatement savings.

Every case is unique, but the value of the abatement makes fighting the clawback worthwhile.

|

|

American Property Tax Counsel

Recent Published Property Tax Articles

The Commercial Property Tax Rebellion

The property tax system in the United States, which traces its roots to colonial America, has long been the life blood of local government finance. Used to fund schools, infrastructure and vital municipal services, it is also a system fraught with controversy and mounting calls for reform.

Over the past...

Read moreHow to Achieve Fair Valuation of Renewable Energy Facilities

As renewable energy assets become more prevalent in commercial real estate portfolios – especially among industrial and data center users – property owners face a critical challenge: ensuring that intangible assets are not mistakenly included in the taxable value of real and personal property.

Wind farms, solar installations, battery energy storage...

Read moreTaxing Real Estate On Redevelopment Prospects

When a property's current use isn't highest and best, New Jersey jurisdictions can assess and tax based on hypothetical redevelopment.

It's hard to imagine a more dystopian world than one in which governments base real estate tax upon a hypothetical use other than a property's current and actual use. Unfortunately, taxing...

Read moreMember Spotlight