"Nearly every state constitution requires uniformity in taxation, meaning that two like properties should receive the same assessment, no matter how they are owned, occupied, built or financed."

Commercial property owners around the country are cheering a recent Pennsylvania Supreme Court decision that breathes new life into constitutional guarantees of uniformity in taxation. Overruling a decade of lower court decisions, the ruling reestablishes the primacy of constitutional uniformity protections to taxpayers in the strongest possible language, fittingly issued just one day after the July 4 holiday.

Nearly every state constitution requires uniformity in taxation, meaning that two like properties should receive the same assessment, no matter how they are owned, occupied, built or financed. Yet commercial property owners across the nation have been under attack by assessors attempting to alter appraisal theory in order to pin higher assessments and higher real estate taxes on specific owners.

These assessors have been singling out occupied commercial properties by setting assessments based on financing mechanisms that fail to meet standard appraisal definitions of market sales, incorrectly basing taxable value on data relating to sale-leasebacks, turnkey leases and contract rights arid duties associated with tenant financing.

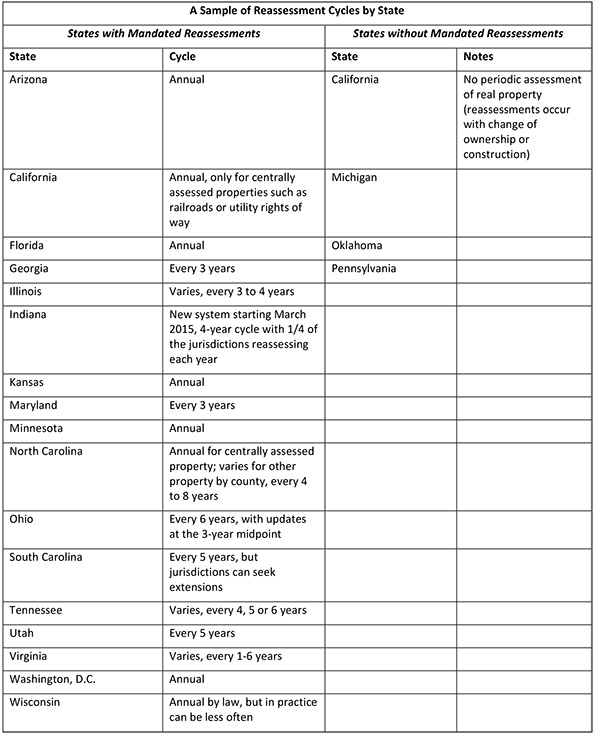

In Pennsylvania and Ohio, the only states that provide school districts a statutory right to file increase appeals, the school districts have been targeting specific commercial owners for higher assessments using this same flawed methodology. These selective or “spot” appeals disrupt constitutionally required uniformity in assessment. Many Pennsylvania school districts have been paying contingency fees to behind-the-scenes consultants to select properties for appeal.

Commercial Portfolio Owners Beware

The consultants’ favorite repeat targets are national real estate portfolio owners that cannot vote in local school board elections. The practice has gained traction over the past five years, with national companies being forced to defend against an ever-increasing number of increase appeals in which school districts seek discovery of the property owner’s confidential real estate information and then use it against the owner to justify an increase in assessment.

This practice violates fundamental fairness and puts targeted commercial owners at a competitive disadvantage with commercial owners whose assessments are not increased. It also shifts more of the tax burden from residential to commercial owners, since most school districts are loathe to sue voting residential owners to increase their assessments.

In Valley Forge Towers Apartments LP vs. Upper Merion Area School District, the school district filed increase appeals only against commercial property owners and not against residential owners. The district selected properties for appeal after consultation with Keystone Realty Advisors, a New Jersey tax consultant that employs trained appraisers and takes a 25 percent contingent fee on any increase in taxes resulting from its recommended appeals.

Four apartment building owners that had been targeted for these appeals challenged the school district’s selection of only commercial owners for appeals as violating the Pennsylvania Constitution’s uniformity in taxation requirement. Both the trial court and the first-level appellate court denied the taxpayers’ challenge, holding that the school districts goal of increasing revenue justified the selective nature of the appeals.

The Pennsylvania Supreme Court reversed those rulings. The court stated that all taxpayers must be uniformly treated, whether they are residential or commercial owners, and that no assessment scheme can systematically treat residential and commercial taxpayers differently.

The court stated no less than 13 times that all real estate is a single class. The court observed that this constitutional tenet has been in place since 1909 and was reaffirmed by the court on multiple occasions, and that the court had no intention of discarding it. The court then stated that the government may not create sub-classifications of property for different tax treatment, a point it repeated nine more times in its decision.

What the Ruling Means Going Forward

The ruling makes it abundantly clear that all real estate must be taxed uniformly, and that this constitutional protection is for the benefit of the taxpayer:

“First, all property in a taxing district is a single class, and as a consequence, the uniformity clause does not permit the government, including taxing authorities, to treat different property sub-classifications in a disparate manner,” the court stated. “Second, this prohibition applies to any intentional or systematic enforcement of the tax laws and is not limited solely to wrongful conduct.”

The court then remanded the case to determine if there was a systematic disparate treatment of the Valley Forge taxpayers. It will be unnecessary to show that the school intended to treat the taxpayers differently from other taxpayers.

The principal takeaway from the case is that all taxes must be uniformly assessed, and that any purposeful or unintentional systematic assessment that treats taxpayers in a disparate manner is unconstitutional.

The Pennsylvania Supreme Court’s decision underscores the need for a real estate taxation standard that treats residential and commercial properties uniformly. In current practice, assessors around the country assess commercial and residential properties using different standards. Residential property is taxed on a fee-simple, unencumbered basis: that is, the property is assumed to be vacant and available for purchase as of the assessment date.

Commercial property, on the other hand, increasingly has been assessed on the assumption that it is occupied by a successful business. In those instances, the assessment reflects the way that the business finances its occupancy, whether it chooses to lease the building or own it outright. Commercial property frequently trades as part of an ongoing business or with long-term leases, deed restrictions or other use restrictions in place. But to be uniform, property taxes must rely upon a single interest valued for tax purposes.

The only interest that is uniform across all categories is the fee-simple, unencumbered value. As the Valley Forge decision makes clear, there can only be one standard because all real estate is a single class.

Now, across the country, tax professionals can use the Valley Forge decision to bring fairness to commercial property owners.