Since the onset of the Great Recession in 2007 the home ownership rate in the United States has fallen by a considerable 4 percent, according to the Census Bureau. While the U.S. may not have become a nation of renters, that long-cherished and widely promoted American dream of home ownership appears to be less attainable and less desirable than it was a decade ago.

This shift in housing demand has sparked a construction boom in the multifamily sector. Across the nation, developers are building a vast amount of multifamily units. According to Cassidy Turley's most recent U.S. Macro Forecast, developers are set to deliver 160,000 new units this year, the most robust construction period in 15 years.

There has been a lot of ink spilled regarding the significance of this sea-change in housing. Often overlooked, though, is the effect this construction boom will have on property taxes in the multifamily sector in general. To understand the implications for property taxes, however, taxpayers must first understand how tax assessors typically value multifamily buildings.

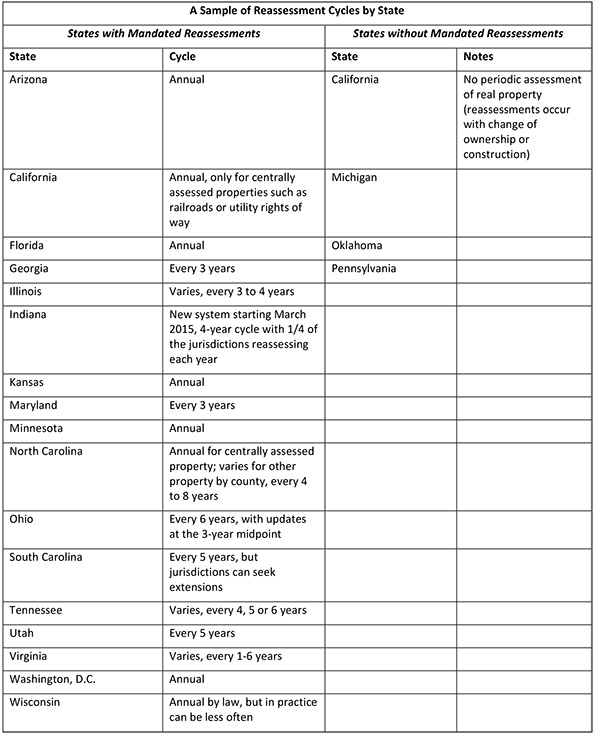

Many tax jurisdictions, including the District of Columbia, employ a computer-assisted mass appraisal (CAMA) system to value multifamily buildings. CAMA systems are designed to simplify the assessment process across a product type, with the goal of producing more uniform assessments, as opposed to property-specific valuations.

To accomplish this, the taxing entity first stratifies properties into different categories and sub-categories. For instance, the D.C. assessor's office first categorizes multifamily buildings as either high-rise (five floors or more) or low-rise (four floors or less). It then further segments properties by submarket; in D.C. there are three general areas.

With properties categorized by the taxing jurisdiction's specifications, the assessor's office enters actual rental, expense and vacancy data for products within each specific category into the CAMA system. The computer model then produces statistical market-based indices for the various categories.

Assessors use these market-based indices to assess individual properties within categories, rather than using rental and expense information that is unique to that property. While adjustments can be made on an individual basis for property-specific issues, the goal of the CAMA system is to produce uniform assessments within the stratification.

Notwithstanding general grievances with CAMA valuations (and this writer has many), CAMA systems are based on general market data, which makes them prone to break down during periods of rapid market change, or when the stratifications are not updated in a timely manner.

One such scenario involves an oversupply at one end of the sector, as is now occurring in many cities due to the construction of class-A multifamily product. Too much construction of class-A apartments can result in lower occupancy levels and downward pressure on rents for these properties. In another, less understood scenario is a process that has been described as "filtering," in which new class-A product, with its higher levels of finish and greater amenities, displaces existing class-A product at the high end of the market. The older, formerly class-A buildings effectively join the class-B category, achieving lower rental rates than the newer product.

In the latter scenario, the stratifications within the CAMA system must be updated in a timely manner to reflect the new market realities. If they are not, the CAMA system will break down as it aggregates data from dissimilar properties, thus resulting in inflated values for the former class-A buildings.

Washington D.C. is beginning to experience the onset of this market dynamic. Research by Delta Associates indicates that while class-A rents rose slightly across the district, they actually decreased in established submarkets with relatively little new product, such as in the Upper Northwest. The district hasn't adjusted its market stratification's to reflect this new phenomenon, however. Instead, the system lumps together markets that have seen decreased rental rates with markets that are experiencing rent growth due to the influx of new class-A product.

Moreover, in the district all high-rise buildings are included in the same pool of comparable properties, regardless of when they were built, or what levels of finish or amenities they offer. Consequently, unless D.C. updates its CAMA system to reflect these new market norms, it is likely that in the next few years we will begin to see the CAMA system overstate assessments for older class-A product.

While taxing jurisdictions should be cognizant of these market changes and make timely adjustments to their CAMA systems, it will often fall to the property owners to be vigilant in monitoring and, when necessary, appealing property assessments. Watching a building's rent levels decrease due to competition from newer product is bad enough—having the city also tax that building as if it were the newer product just adds insult to injury.