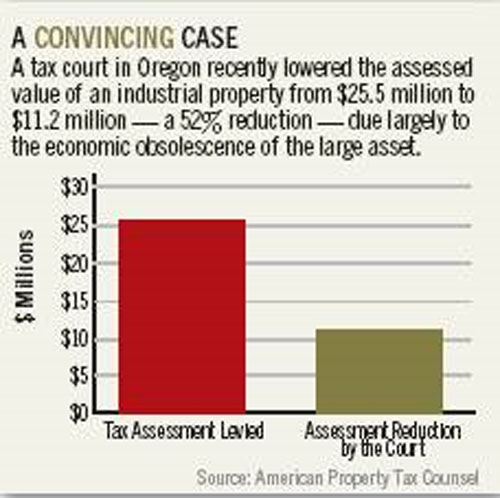

"Despite the law, there appears to be one abiding maxim that all tax assessors observe: Every high sale price represents a market value sale, and every low sale price is seen as a distress sale."

New Jersey, as in most other jurisdictions in the US., all real property must be valued and assessed based on market value. It's the law. Market value is defined as the price paid by a willing buyer to a willing seller, each acting knowledgeably, without duress.

Despite the law, there appears to be one abiding maxim that all tax assessors observe: Every high sale price represents a market value sale, and every low sale price is seen as a distress sale. Further, every high sale can be relied upon to set an assessment and every low sale must be disregarded because it took place under distress. However, the real issue revolves around: Is every sale a market event that represents fair market value for assessment purposes? The Tax Court of New Jersey has focused on this issue and determined that a category of events exists that rule out a sale as a reliable indicator of fair market value for assessment purposes.

A transaction set up as a 1031 tax-free exchange represents one such category identified by the Tax Court. Under 1031, sellers of investment-grade real estate may defer paying capital gains by using the proceeds from one sale as an investment in another similar property or properties. The seller has 180 days from the original closing date to complete the exchange. Also, within 45 days of closing, the taxpayer must provide the IRS a list of three or more potential replacement properties.

In a recent case, the Tax Court agreed with the taxpayers arguments that his 1031 sale price was significantly higher than market value. The court concluded that the sale price was motivated by tax and business issues rather than typical real estate motivations. The court also concluded that the tax free exchange laws placed enormous pressure on a seller to conclude a transaction within 180 days. Fundamentally, the sale took place primarily to defer gains from another sale.

Another category of sales rejected by the Tax Court compromise those that have not been properly marketed. For example, a Fortune 500 company sold a corporate headquarters for $16 million. The sale was conducted via sealed bids over a short period of time. The bid package included language that prohibited the bidders from changing any of the sale terms. The court determined that the bid package was not sent to all potential buyers. As a result of these perceived defects in marketing the property, the court rejected the sale price and concluded to a market value of $49 million.

In contrast to the prior set of facts, the Tax Court has also concluded that the sale of a complex property can be market value. In another case, an oil refinery was sold after it was marketed for more than 18 months. The owner hired an investment banker to market the property. The investment banker identified all of the potential buyers. Comprehensive information packages identifying the property were transmitted all over the world. At the end of this marketing period, the seller received two bids, eventually resulting in a sale. The court concluded that such a significant amounted to a valid sale that could be used to value the property for tax assessment purposes.

Some of the same arguments made with regard to 1031 property can also be advanced for high purchase prices paid by REITs. REITs offer significant tax advantages to shareholders; however, they must meet strict tax requirements in order to qualify for that status. A RElT must distribute 90% of its income to shareholders. Thus, in order for a RElT to grow, it must continually purchase properties, as it cannot grow via the normal accumulation of cash.

Growth is critical because it leads to higher stock prices and allows for more diversification in the portfolio. Additionally, REITs use capital markets to which most other buyers do not have access. These large capital markets fund REIT purchases at low interest rates that further the aims of the REIT. All of these issues would normally cloud the price paid by a "willing buyer, acting without duress."

In an era characterized by unusually high sales prices, tax payers need to remember an important caveat: Even the New Jersey Tax Court recognizes that not every sale represents fair market value for tax assessment purposes. Owners involved in transactions with high sales prices need to carefully examine their property tax assessments to determine whether a valid market price was used in levying their assessment.

Not only are the rents affected by the first-generation tenant, the capitalization rate is significantly lower than market rates. The net-lease market into which these properties are sold is among the most active and developed in the real estate market, allowing for substantial liquidity, efficient pricing, and tax deferral through 1031 exchanges.

Not only are the rents affected by the first-generation tenant, the capitalization rate is significantly lower than market rates. The net-lease market into which these properties are sold is among the most active and developed in the real estate market, allowing for substantial liquidity, efficient pricing, and tax deferral through 1031 exchanges.

The business value reflects all the factors of production —— land, buildings, machinery and equipment, skilled labor, managerial expertise and goodwill. It is incumbent upon owners to show assessors how to separate the value of the real and personal property from the value of the business for assessment purposes.

The business value reflects all the factors of production —— land, buildings, machinery and equipment, skilled labor, managerial expertise and goodwill. It is incumbent upon owners to show assessors how to separate the value of the real and personal property from the value of the business for assessment purposes.

Just because your local assessor relied on comparable sales to give your property a higher valuation and a bigger tax bill doesn't mean you should pony up without a fight. Take a look at the comps and see how comparable they really are: You may be able to successfully argue that properties built recently, featuring larger unit sizes, or selling with Effective local tax assumable financing were able to fetch much higher sales prices than your property rates are a critical could reasonably command.

Just because your local assessor relied on comparable sales to give your property a higher valuation and a bigger tax bill doesn't mean you should pony up without a fight. Take a look at the comps and see how comparable they really are: You may be able to successfully argue that properties built recently, featuring larger unit sizes, or selling with Effective local tax assumable financing were able to fetch much higher sales prices than your property rates are a critical could reasonably command.