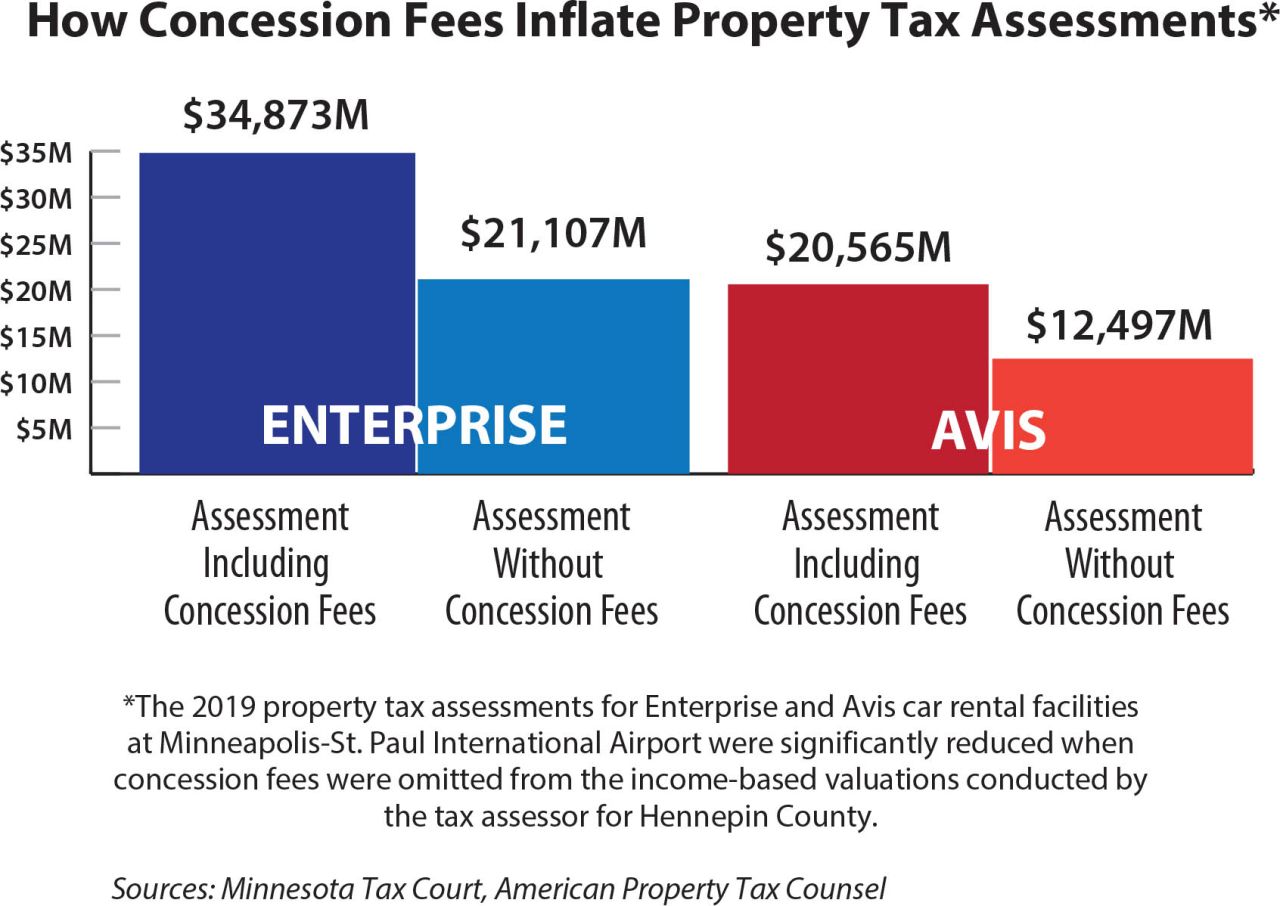

Here are some property tax strategies owners can use in the rebounding apartment sector.

Multifamily construction and renovations are enjoying a resurgence after taking a pause during the pandemic. And with residential, apartment-style rental units back in vogue with renters and investors, developers are even converting underutilized office buildings and shopping malls into multifamily housing.

As developers step up construction spending to tempt renters with an assortment of amenities, tax assessors are having a field day, tabulating costs on renovations and new projects that they are using to justify ever-larger assessments of taxable value across the sector. Multifamily owners must look out for themselves to guard against unfair, blanket assessment increases founded on these gross generalizations about the industry.

New offerings, New Renters

The target demographics for today's projects include young professionals not yet equipped to buy their own homes; middle-aged, single-family homeowners looking for a more carefree housing option; and aging individuals looking to downsize and become part of a seniors community.

Apartment models have evolved to better suit today's renters. Gone are the cookie-cutter, brick-and-mortar, garden style structures with minimal common areas. New apartment communities are more often high-end projects boasting pools, gyms, lush landscaping, retail shops and other non-traditional apartment features.

The added expense to deliver amenity-rich apartments is only one of many rising costs for multifamily developers and owners. Supply chain breakdowns, material shortages, rising interest rates on commercial mortgages, governmental bureaucracy, and increased inflation have forced owners of apartments and other commercial buildings to search for avenues to reduce their costs. While costs associated with owning and maintaining apartment buildings are trending higher, real property taxes remain one of the largest expenses, warranting an annual review and challenge.

Fortunately, in ad valorem jurisdictions where a property's tax assessment is tied to its market value, the law allows taxpayers to appeal assessments and seek relief from onerous real estate taxes. The process involves the filing of an annual administrative grievance followed by a judicial action against the tax-assessing entity.

The Protest Process

In tax appeal proceedings, the aggrieved party or petitioner bears the initial burden of proof. Assessments are presumptively valid, so it is up to the taxpayer to provide substantial evidence that calls into question the assessment's correctness. Taxpayers often meet this minimum standard by submitting a qualified appraisal.

In a court setting, once the presumption of validity is rebutted, the judge must determine by a preponderance of the evidence whether the property was overvalued. However, most tax assessment cases reach a resolution through negotiation and settlement without the need for a formal expert report or judicial oversight. A tax advisor skilled in real property tax assessment challenges is more often than not all the taxpayer requires.

The three traditional approaches to real property valuation in a tax appeal are the income capitalization, comparable sales, and cost approaches. Absent a recent arm's-length sale of the subject property, appraisal professionals, practitioners, and the courts generally regard income capitalization as the preferred method to value income-producing properties.

In utilizing the income approach, a taxpayer's team is seeking to value the property based on its net-income-generating potential. In other words, what would a buyer pay on the valuation date for the future income stream?

Point-by-Point Analysis

There are several steps to properly arrive at a value conclusion through the income approach. Understanding and following the steps will not only inform the property owner's valuation, but also provides a checklist to review and question calculations in the assessor's conclusion.

To calculate potential gross income, it is important to analyze the subject property's actual rental data and test it against market rents to reflect the property's economics. Similarly, the assessor or appraiser must gather, review and analyze occupancy and collection data. The appraiser will need to deduct for vacancy and collection loss because many buildings are seldom at 100 percent occupancy, and some tenants may be behind in their rent payments.

The same process is applied to real estate-related expenses such as insurance, utilities, and replacement reserves. These should be deducted to arrive at a net operating income before the deduction of real estate taxes.

In analyzing data for a tax assessment challenge involving income-producing property, real estate taxes are not accounted for at this stage because this is the expense in question. In addition, since the property tax expense is a percentage of market value, it is accounted for in the capitalization rate along with an appropriate rate of return reflecting the risk of investment.

Appeal prospects

How can the taxpayer gauge a tax appeal's likelihood of success? Among other things, consider the size of the rental units, location, competition, and parking to form a reliable value opinion. Give special attention to the tax system in the state and local jurisdiction where the property is located to ensure the taxpayer meets all statutory filing requirements and deadlines. If a challenge is not timely and properly commenced, the aggrieved party will lose its right to real property tax relief for that tax year.

Given the complexity of commercial property valuations and the nuances involved in disputing the correctness of valuation calculations, savvy apartment building owners may benefit by discussing their property's economics with a specialist in real property tax assessment review challenges.