Using comparable market sales for taxation can correct errors assessor errors.

"The tax professionals' initial work identified three relatively recent sales of comparable properties that suffered from functional and external obsolescence, much like the taxpayer's property."

Assessors typically value industrial and commercial properties using a cost approach that starts with land value, adds the cost of property improvements and subtracts some physical depreciation, often based on the property's age. Deducting only the physical depreciation from a property tax valuation often results in egregiously excessive taxation. However, by applying data regarding comparable market sales, taxpayers can remedy this problem, sometimes with extraordinary results.

Seldom are such factors as functional or external obsolescence, which can dramatically diminish property values, used in assessors' property tax valuations. Functional obsolescence arises from the flaws that exist in a property. Examples include an abnormal size, shape, or height, concrete floors that are exceptionally deep or too shallow and so forth.

External obsolescence results from outside forces such as industrial properties becoming vacant because production moves offshore, or a change in tax laws that reduces commercial property values. Fortunately, data from comparable property sale can be used to identify specific amounts of functional and external obsolescence; amounts that must be deducted from assessors' valuations to eliminate unlawfully excessive taxation.

Consider an industrial facility with above market operating expenses that houses manufacturing barely surviving global competition. In an actual case similar to this example, the assessor made a mere 4% reduction for functional and external obsolescence even after the taxpayer had fully described the obsolescence. Ultimately the taxpayer retained property tax professionals who knew how to use sales of comparable properties to demonstrate the diminished values the obsolescence caused.

How the process works

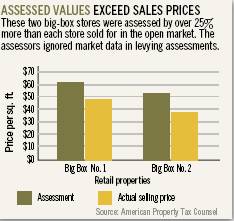

Assessor's records commonly contain errors in a property's age, total square footage, net leasable area, number of units, unit mix, and facility amenities. An error in the property's basic data can significantly increase a property's overall assessment. Providing a current rent roll to the assessor can help correct mistakes in a property's basic data. An owner may also wish to produce a site plan for the property along with the most recent marketing materials that show the project's different floor plans and amenities. Correcting basic errors in the assessor's records remains the simplest path to lower a tax assessment.

The tax professionals' initial work identified three relatively recent sales of comparable properties that suffered from functional and external obsolescence, much like the taxpayer's property. The professionals used these sales to quantify depreciation in a way that enabled them to reasonably estimate the obsolescence in the taxpayer's property. Using the steps followed by the professionals, taxpayers can garner stunning property tax reductions. Here's how:

- Determine the value of improvements by subtracting the value of the land from its sale price for each of the comparable properties.

- Determine the construction cost of improvements when new by researching construction costs in national estimating services such as Marshall Valuation.

- Calculate the property's total depreciation by subtracting the value of the improvements today from the cost to construct the improvements.

- Ascertain physical depreciation by dividing the property's effective age by its life expectancy.

- Estimate functional and economic obsolescence by subtracting the physical depreciation from its total depreciation.

The taxpayer's reward

Completing this analysis for the three comparable sales produced an indication of functional and external obsolescence that was far greater than the assessor recognized in his assessment. Having established a 40% to 48% range for obsolescence, the professionals then determined whether any further adjustments were warranted such as those due to differences between the sold properties and the taxpayer's property.

For example, unlike the sold properties, the taxpayer's property was both excessively large and had an unusual shape. These features would cause the taxpayer's property to suffer from even greater obsolescence than the sold properties.

As a result of the analysis, the assessor agreed that a proper cost approach required both the physical depreciation originally calculated plus an additional 40% reduction for obsolescence, an $8 million assessment reduction.

This example demonstrates that the property owner was able to deduct functional and external obsolescence without relying on an income analysis. In this case, property was located in a market where virtually all of the industrial properties were either owner occupied or vacant, making it impossible to obtain income information.

In the cost approach, where physical depreciation represents the only deduction, taxpayers should expect that properties with functional and external obsolescence will be overvalued.

When that happens it is crucial that taxpayers take action. To paraphrase the renowned philosopher, Mick Jagger, when it comes to property taxation, taxpayers may not be able to get what they want, but armed with the right information and professional assistance, they may be able to get what they need.

Not only are the rents affected by the first-generation tenant, the capitalization rate is significantly lower than market rates. The net-lease market into which these properties are sold is among the most active and developed in the real estate market, allowing for substantial liquidity, efficient pricing, and tax deferral through 1031 exchanges.

Not only are the rents affected by the first-generation tenant, the capitalization rate is significantly lower than market rates. The net-lease market into which these properties are sold is among the most active and developed in the real estate market, allowing for substantial liquidity, efficient pricing, and tax deferral through 1031 exchanges.