Property Tax Resources

Big Boxes and Industrial Plants Unfairly Taxed

Assessors' misuse of highest and best use principle proves costly.

"To support inflated values, taxing units attempt to narrowly define the highest and best use of the property."

In many states, the war over property tax assessments based on "value to the owner" as opposed to "market value" has ended with a clear victory for market value. Nonetheless, some jurisdictions continue to try changing this outcome by misusing "highest and best use."

Assessors' attempts to misuse highest and best use can be seen most often in buildings used by big-box retailers and manufacturers, as opposed to properties such as hotels, office buildings and shop-

ping centers, typically valued using the income approach.

To support inflated values, taxing units attempt to narrowly define the highest and best use of the property. They claim that a taxpayer's comparable sales aren't evidence of market value because the sale properties have a different highest and best use than the property being assessed.

Two methods, two results

An assessor may contend, for example, that only stores purchased by Jones Corporation can be used to value a store used by Jones Corporation. This effectively eliminates comparable sales as a basis for valuation. One tax court addressed this issue when it held that a property's highest and best use cannot be defined "so narrowly that it precludes analysis and value based on market data."

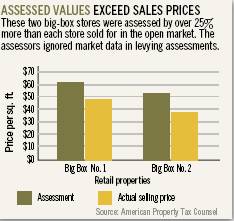

The accompanying chart demonstrates the difference between the assessor's valuation of two big-box stores based on his narrow definition of highest and best use and the actual selling price of those same stores in the open market.

The assessor defined highest and best use as that use being exercised by that specific retailer. That definition led the assessor to value big-box store No. 1 at $62 per sq. ft. and big box store No. 2 at $58 per sq. ft. Actually, store No. 1 sold to another retailer for $49 per sq. ft. and store No. 2 was bought by a different retailer for $38 per sq. ft.By narrowly defining highest and best use, the assessor ignored market data and over assessed the property.

The relevance of a comparable sale's highest and best use was addressed in the case of Newport Center v. City of Jersey City. The New Jersey Tax Court held that a comparable sale should be admissible evidence of value, regardless of its highest and best use, if the claimed comparable sale provides logical, coherent support for an opinion of value.

Many jurisdictions want to effectively reinstate value to the owner, in legal terms called "value-in-use," as the lawful standard for property tax valuations, thereby inflating assessments by eliminating from consideration the sales-comparison approach to value. In the sales comparison approach, sales often provide the best indication of a big box or manufacturing property's market value.

Sales prices reflect loss in value from replacement cost due to obsolescence. That obsolescence generally includes a significant amount of external obsolescence, which represents loss in value caused by some negative influence outside the property.

For example, external obsolescence could result from limited market demand for a big-box store or manufacturing plant built to meet the needs of a specific user. Value may also be adversely influenced by functional obsolescence, a loss in value due to design deficiencies in the structure, such as inadequate ceiling heights, bay spacing or lighting.

What's a comparable sale?

Appraisers are taught to only use sales comparables with the same or similar highest and best use to that of the property being appraised. However, even this limitation is too restrictive.

For example, years ago a former automobile assembly plant was offered for sale and eventually sold for demolition and construction of a shopping center. No automobile manufacturer, or for that matter any other manufacturer, was willing to pay more for this property than the developer who bought it to build a shopping center.

Thus, the market spoke and defined the market value of the former automobile plant. In short, if a property is physically similar to the property being valued, but sells for an unusual use, that sale should not necessarily be disregarded as a comparable sale.

The sale of the former automobile assembly plant for use as a shopping center may not be the ideal comparable sale to value industrial property. However, that sale certainly puts a cap, or limit, on the value of a similar industrial facility, subject of course to adjustments for relevant differences such as location or size.

By understanding the issues involved in using comparable sales to achieve market value assessments, taxpayers can successfully appeal property tax assessments when they are based on the misuse of highest and best use.

American Property Tax Counsel

Recent Published Property Tax Articles

The Commercial Property Tax Rebellion

The property tax system in the United States, which traces its roots to colonial America, has long been the life blood of local government finance. Used to fund schools, infrastructure and vital municipal services, it is also a system fraught with controversy and mounting calls for reform.

Over the past...

Read moreHow to Achieve Fair Valuation of Renewable Energy Facilities

As renewable energy assets become more prevalent in commercial real estate portfolios – especially among industrial and data center users – property owners face a critical challenge: ensuring that intangible assets are not mistakenly included in the taxable value of real and personal property.

Wind farms, solar installations, battery energy storage...

Read moreTaxing Real Estate On Redevelopment Prospects

When a property's current use isn't highest and best, New Jersey jurisdictions can assess and tax based on hypothetical redevelopment.

It's hard to imagine a more dystopian world than one in which governments base real estate tax upon a hypothetical use other than a property's current and actual use. Unfortunately, taxing...

Read moreMember Spotlight