Next Tuesday Michigan voters will decide whether to approve the phase out of personal property taxation involving small assessments and industrial taxpayers. Specifically, the ballot question asks whether a portion of the state's use tax should be assigned to local governments to reimburse them for tax revenues no longer collected on personal property. If the ballot question fails, the entire phase-out plan will be repealed.

The personal property exemption for small assessments actually started in 2014. Businesses with personal property having a true cash value of $80,000 or less in a particular assessing jurisdiction could claim an exemption for that property. If a business owned, leased or was in possession of personal property with a true cash value of more than $80,000 in that jurisdiction, the full tax was owed. Under the plan, taxpayers must file an affidavit with the local assessor each year by February 10 to claim the exemption for personal property with a true cash value of $80,000 or less. In a few instances this year, we did see assessors ask to see calculations using the State Tax Commission valuation tables to verify the exemption claim. If the voters approve the phase-out there could be such requests in the future.

The phase-out plan provides that industrial personal property placed into service after December 31, 2012 will become exempt in 2016. Any industrial personal property in place for at least 10 years will also be exempt. As a result, in each tax year after 2016 a new vintage year of industrial personal property will become exempt until all industrial personal property is exempt by 2023.

Proposal 1, even if enacted, does not completely eliminate the tax on personal property. Commercial personal property that is not otherwise exempt and utility personal property will remain taxable. In addition, the plan includes and is not currently limited to a state levied, special assessment on industrial personal property. The special assessment will be imposed on certain industrial personal property and will equate to approximately 20% of what the tax would have been if the personal property were not exempt.

Legislature to consider changes to tax appeal procedure

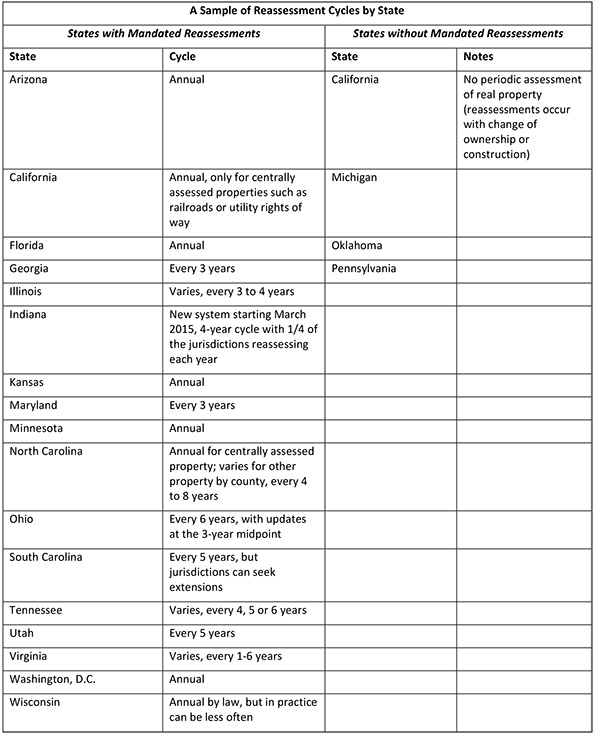

A state senator is proposing a number of changes to the property tax appeal process. The proposed changes include moving the annual appeal deadline to July 31 for all types of property (the current deadline is May 31 for commercial and industrial property). Proposals also include allowing 60 days to appeal administrative rulings, standardizing the appeal processes for various exemptions and allowing petitions for the correction of assessment errors to include the current year and three previous years. The Legislature will be pressed to address all of these issues before the end of the year, but at least some of them may well get a hearing and could be enacted this year.

For more information regarding this alert or any another property tax appeals related issue, please contact any of our Tax Appeals attorneys.

Last week Michigan voters overwhelmingly approved Proposal 1. While Proposal 1's passage will significantly reduce or eliminate personal property taxes for many Michigan businesses, contrary to some articles, it will not eliminate Michigan personal property taxation. The program consists of a phase-out of the tax on certain industrial and industrial related personal property. In addition, there is an exemption for businesses with small amounts of personal property in a given locality.

"Small Business Exemption"

Starting in 2014, businesses with personal property having a true cash value of less than $80,000 in a particular assessing jurisdiction can claim a personal property exemption for that property. If a business or a related entity owned, leased or was in possession of personal property with a cumulative true cash value of $80,000 or more in that jurisdiction, then the full tax is owed. Under the plan, taxpayers must file an affidavit with the local assessor each year by February 10 to claim the exemption for personal property with a true cash value of less than $80,000. If the claim is based on a valuation method that differs from the State Tax Commission's valuation tables, then the claimant must explain the method used. However, if the required affidavit is filed, the taxpayer does not have to file a personal property statement for that tax year. Claimants are subject to audit and must maintain adequate records for at least 4 years from the year the exemption was claimed. If a claim for exemption is denied, then the taxpayer may appeal to the local Board of Review and then the Michigan Tax Tribunal.

Industrial Processing and Direct Integrated Support Equipment

In 2016, a phase out of the personal property tax on Industrial Processing and Direct Integrated Support Equipment will begin. This exempt equipment is referred to as Eligible Manufacturing Personal Property (EMPP). EMPP placed into service after December 31, 2012 will become exempt in 2016. Going forward, any EMPP in place for at least 10 years also will be exempt. As a result, in each tax year after 2016 a new vintage year of EMPP will become exempt until all EMPP is exempt by 2023.

The exemption could be determined on a parcel-by-parcel basis, or a group of contiguous parcels. If over 50% of the original cost of the personal property on a parcel or group of contiguous parcels is used in industrial processing or direct integrated support, then the whole parcel or group is exempt. Use in industrial processing is determined by whether the asset would qualify for the industrial processing exemption under the Michigan Sales/Use Tax Acts. Direct Integrated Support involves functions related to industrial processing including R&D, testing and quality control, engineering, as well as some warehousing and distribution activities.

Taxpayers will be requested to file a form in 2015 estimating the amount of personal property they plan to claim for exemption for the 2016 tax year. If that form is filed, then the taxpayer will only have to file for the exemption in the first year (not each subsequent year) and will not be required to file personal property tax returns on the exempt parcels.

State Essential Services Assessment

The plan also creates a State Essential Services Assessment (SESA) which begins in 2016. The SESA is a special assessment applied to EMPP and used to offset some of the revenues lost from the new exemption. Generally, the SESA will amount to about 20% of what the tax would be if the EMPP were not exempt. An electronic filing and full payment to the Department of Treasury will be due by September 15 of each year. If payment is not made by November 1, then the tax exemption will be revoked.

Other Exemptions

The plan also addresses EMPP that is already exempt under other statutory provisions, including PA 198 industrial abatements and PA 328 personal property exemptions. Exemption certificates under these acts for EMPP that were in place prior to 12/31/12 will be automatically extended to the year that the EMPP would otherwise become exempt. For example, a twelve year PA 198 abatement for EMPP that was set to expire on 12/30/13 will now be extended to 12/30/15. Such a PA 198 abatement would expire at the end of 2015, but the EMPP will become exempt in 2016 under the new law. Also, the SESA will apply to some EMPP that is subject to PA 198 or PA 328 depending on which exemption applies and the date the certificate became effective.

As Proposal 1 is implemented, undoubtedly there will be many questions and issues that arise.

If you would like further information about this client alert or any other tax appeals related issue, please contact:

Scott Aston

313.465.7206

saston@honigman.com

Sarah R. Belloli

313.465.7220

sbelloli@honigman.com

Mark A. Burstein

313.465.7322

mburstein@honigman.com

Jason S. Conti

313.465.7340

jconti@honigman.com

Aaron M. Fales

313.465.7210

afales@honigman.com

Carl W. Herstein

313.465.7440

churstein@honigman.com

Mark A. Hilpert

517.377.0727

mhilpert@honigman.com

Jeffrey A. Hyman

313.465.7422

jhyman@honigman.com

Leonard D. Kutschman

313.465.7202

lkutschman@honigman.com

Stewart L. Mandell

313.465.7420

slmandell@honigman.com

Steven P. Schneider

313.465.7544

sschneider@honigman.com

Michael B. Shapiro

313.465.7622

mshapiro@honigman.com

Daniel L. Stanley

517.377.0714

dstanley@honigman.com