Tips to help affordable housing owners control their tax burden

"Being a unique property type established largely as a creature of government funding/subsidy programs, affordable housing assessment challenges should not take a cookie-cutter approach."

When it comes to property tax considerations for affordable housing, one expert summed it up well. He wrote: "Opinions on the proper assessment of affordable housing real property are varied, and decisions on the best method to use in developing these assessments vary from jurisdiction to jurisdiction."

Thus, controlling the tax burden of affordable housing properties is a difficult matter about which to generalize. However, based on available guidance and experience, a number of questions should be researched by owners in all jurisdictions:

- Is there a state statute of general application that addresses the valuation of affordable housing for ad valorem purposes? If so, is the statute applicable to the type of financing/subsidy arrangement in place at the property? For example, what income or asset tests must be met by residents for the project to qualify?

- Has the local assessment authority issued any regulations dealing with this issue?

- Has a state agency with oversight authority over the local assessment practices carried out its duties?

- What restrictions are imposed on the owner? How long are these restrictions in place?

- If the nature of the financial benefit derives from mortgage financing, when do these restrictions expire?

- How have the courts of the applicable jurisdiction ruled on valuing these properties? What are the reported decisions from the highest appellate court or various trial courts?

Finding highest and best use

With those questions in mind, let's look at the approaches to real estate valuation: costs, sales, and income. With each methodology, determination of value requires understanding, first, and concluding what the highest and best use may be.

In this analysis, the highest and best use finding must be able to include the fact that the property is in some fashion or other rent-restricted and/or return on investment (ROI) limited and dependent on the government subsidy, guaranty, or concession for its creation and ongoing existence.

The cost approach is usually not helpful to value an affordable housing property. For older developments, depreciation and obsolescence generally become difficult to measure. For newer properties, construction cost is irrelevant unless the same government subsidy or program can be determined to be in place to support a new property. In these economically stressed days, that assumption may not hold.

The sales approach contains many of the same deficiencies since most market transactions will not be government-subsidized properties, but rather market-rate projects. Affordable housing projects tend not to trade frequently. By the same token, lack of comparable rent structures and locations will usually render the sales approach of little help.

In most circumstances, the income approach is the best methodology. As Richard E. Polton, MAI, points out, a property in the early years of its rent/net operating income (NOI) restriction covenants is probably best valued using a direct capitalization methodology. However, he continues, a project nearing the end of these restrictions, with a reasonable opportunity to revert to a market rental structure, might be better valued using a discounted cash flow approach.

In order to keep property assessment (and therefore taxes) as low as possible, a very careful analysis of the regulatory regime in place must be undertaken by the expert appraiser. Extraction of relevant provisions from the project documents, which support the restricted rent/NOI theme, usually constitutes a wise approach. Inclusion of applicable federal/state statutes and regulations to support the highest and best use conclusion will make the appraiser's report more credible and readable.

What's the cap rate?

Since the NOI of an affordable housing project should be fairly easy to establish, the key analytical challenge becomes developing and supporting a cap rate in order to express the correct market value.

The most convincing data are cap rates extracted from the sales of other affordable housing projects. If sales cannot be located in the immediate or surrounding jurisdictions, regional or national data should be obtained and examined since many larger affordable housing developments trade in the national market. This national activity typically takes place after the original developer extracts development fees and any applicable tax credits for itself and its investors.

Many experts do not think cap rates derived from market sales of non-restricted properties are terribly relevant in developing rates for income/NOI-restricted units. While restricted projects tend to be perceived as carrying lower risk due to assured income streams, appreciation is nonexistent, and major value upgrading potential such as condo conversion is usually impossible. Therefore, non-restricted properties as a group tend to sell at lower cap rates, meaning higher unit values because of the far greater upsides. Affordable housing owners should determine whether the assessing jurisdiction has attempted to place a separate value on the federal housing assistance contract, low interest rate mortgage, or rent subsidy. While these efforts may inflate value, they usually fail to meet state assessment law requirements, which reject adding the value of intangible financial assets to real estate assessments. In most jurisdictions, an attack on the effort by the authorities to assess intangibles will produce a winning assessment appeal.

The devil's in the details

Everyone would agree that a "fair" assessment should be accepted by an affordable housing project. The "devil" of achieving this goal is in the nitty-gritty associated with relating assessments to the ability of a property to carry a particular tax load.

An owner's inability to pass tax increases through in the form of rent subsidy increases or other financial offsets frequently can convince the assessor to reduce his or her expectations. In one circumstance, a tax professional found it very helpful in the prosecution of an affordable housing tax appeal to ask the owner to send leaflets to the property's 300-plus elderly residents about the tax increase concerns. The dozens of letters to the local assessor expressing concern about potential rent increases presumably had some impact in enabling the case to be settled.

Owners should also review for compatibility and consistency the assessments of affordable housing in their jurisdiction or neighboring communities. Occasionally, a tax appeal asserting lack of equalization will be victorious.

Being a unique property type established largely as a creature of government funding/subsidy programs, affordable housing assessment challenges should not take a cookie-cutter approach. An intimate knowledge of the property, applicable financing and restrictions, and market conditions become critical to keeping an assessment under control and thereby bringing taxes down. In the absence of legally binding guidelines or assessment practices and protocols applicable to affordable housing projects, an owner seeking assessment justice has much homework to do.

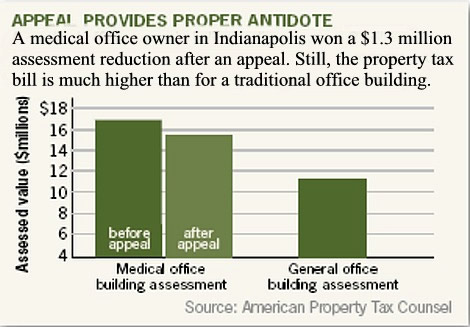

As a result of this painstaking development and presentation of the relevant facts, the Appeal Board ruled in favor of the taxpayer and reduced the property's valuation by $1.3 million to $15.6 million. While this reduction was warranted, the medical office building remains valued higher than the general office building, proving that medical office buildings pay higher property taxes.

As a result of this painstaking development and presentation of the relevant facts, the Appeal Board ruled in favor of the taxpayer and reduced the property's valuation by $1.3 million to $15.6 million. While this reduction was warranted, the medical office building remains valued higher than the general office building, proving that medical office buildings pay higher property taxes.

An owner or property manager examining the rental income from the office property above can rest easy because it's clear that no problem exists. Here's a well-managed property fully leased in a weak economy. However, taxpayers must not be lulled into ignoring the need for a review of any tax assessment received in an economy under duress.

An owner or property manager examining the rental income from the office property above can rest easy because it's clear that no problem exists. Here's a well-managed property fully leased in a weak economy. However, taxpayers must not be lulled into ignoring the need for a review of any tax assessment received in an economy under duress.