"If home price drops, so should property taxes. Home owners might be smart to initiate a property tax appeal."

In these uncertain times, many home owners have had to face the fact that the current market value of their homes is less than they once thought.

Yet, most of these home owners continue to pay property taxes based on that higher value.

Higher taxes may also make a property less appealing and affordable to buyers, since higher taxes will increase their overall costs, at least until the property is reassessed. That's why it's a smart strategy to advise past clients who might be considering a sale to appeal their property taxes at the next opportunity.

Evaluating Your Assessment

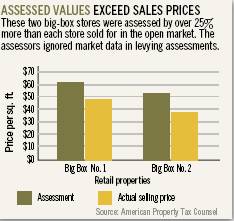

The vast majority of taxing jurisdictions throughout the United States assess residential property based on market value: the amount a willing buyer would pay a willing seller without duress. However, assessments are generally not reviewed on an annual basis, so a property's assessment will never be 100 percent of market value.

To compensate, taxing bodies apply an equalization ratio, which is designed to ensure that assessments are relatively equal among different taxing districts to all assessed values. For example, a property worth $100,000 with an equalization ratio of 50 percent would be assessed at $50,000. Home owners can obtain their equalization ratio from local taxing authorities.

If, after a review with a residential broker or appraiser, a home's assessed value seems out of line with current market values, the home owner should undertake an investigation to determine what might have caused the incorrect valuation. Here are some steps for your client to follow.

- Arrange a visit with the local tax assessor and request a complete copy of the home's tax records. Property record cards are public records and are universally available.

- Pay particular attention to the market comparables listed on the property record card. These recently sold homes are the basis for the assessor's valuation of your client's home. Visit those houses or view them online, and compare them to the client's house.

- Take the appropriate equalization ratio and multiply the market value you believe appropriate for the home by that rate. If the number is lower than the current assessment, your client should file a tax appeal.

Filing an Appeal

Most home owners should be able to properly file the appeal without counsel, but most jurisdictions require a licensed real estate appraiser to prepare an expert analysis of local market values for the local tax board.

Home owners should work closely with the appraiser to review all the amenities and issues that might affect the valuation of their home. Many times an appraiser may not be aware of construction, zoning, or general neighborhood issues that negatively affect value.

Real estate brokers familiar with the property and the area may also be a valuable resource for this type of information. They may also be able to assist the appraiser in determining which properties are the best comparables for a particular home. All of the appraiser's conclusions need to be properly documented with supporting evidence in the appraisal report that will be submitted with other supporting paperwork prior to the hearing.

In addition to compiling evidence, the taxpayer should take care to learn and follow the rules of the local board of assessment review. Each taxing jurisdiction has appropriate appeal forms. It is also critical to determine the deadline for filing an appeal.

The final step in an appeal is a hearing before the assessment appeal board. Proper preparation is the key to a successful hearing. The home owners and the appraiser should prepare a script detailing the important points that need to be made during the appraiser's testimony in order to prove a lower market value and assessment.

The key focus should be comparing the home in question with every presented comparable. The appraiser should be prepared to analyze each important amenity and discuss how it positively or negatively affects value.

During uncertain economic times, the effort of appealing a property tax bill reduction may prove well worth the time and effort involved.

An owner or property manager examining the rental income from the office property above can rest easy because it's clear that no problem exists. Here's a well-managed property fully leased in a weak economy. However, taxpayers must not be lulled into ignoring the need for a review of any tax assessment received in an economy under duress.

An owner or property manager examining the rental income from the office property above can rest easy because it's clear that no problem exists. Here's a well-managed property fully leased in a weak economy. However, taxpayers must not be lulled into ignoring the need for a review of any tax assessment received in an economy under duress.

Assessors typically value golf courses using a cost approach. That approach starts with land value, adds the cost of property improvements, and subtracts physical depreciation. Assessors prefer the cost approach because the availability of cost data from national valuation services makes the determination of a value rather straightforward.

Assessors typically value golf courses using a cost approach. That approach starts with land value, adds the cost of property improvements, and subtracts physical depreciation. Assessors prefer the cost approach because the availability of cost data from national valuation services makes the determination of a value rather straightforward.

Not only are the rents affected by the first-generation tenant, the capitalization rate is significantly lower than market rates. The net-lease market into which these properties are sold is among the most active and developed in the real estate market, allowing for substantial liquidity, efficient pricing, and tax deferral through 1031 exchanges.

Not only are the rents affected by the first-generation tenant, the capitalization rate is significantly lower than market rates. The net-lease market into which these properties are sold is among the most active and developed in the real estate market, allowing for substantial liquidity, efficient pricing, and tax deferral through 1031 exchanges.