One of the bright spots that have emerged in the real estate market over the past five years of the economic recovery has been the multifamily rental segment. Of the 49 major metropolitan markets tracked by Cassidy Turley, only 17 have a multifamily vacancy rate above 5% and only two have a vacancy rate above 7%, according to the Firm's US Multifamily Forecast Report for Summer 2013.

Rental rates have increased in virtually all markets, with the strongest growth in top-tier cities. In Chicago, for example, rents at class A buildings have increased 21% since 2009. And at the national level, multifamily transaction volume quadrupled between 2009 and 2012. Despite these robust indicators, however, some observers worry that the industry may be overestimating the extent of the US multifamily recovery, and that developers are setting the stage for the next bubble.

Since 2012, construction has come to the fore. Almost 60,000 new multifamily units are expected to reach completion by the end of 2013 in the top 10 markets. The bulk of the new construction is class A buildings, which feature amenities such as a doorman, concierge services, work-out facilities, pools and in-unit washers and dryers.

Millenials, born between the mid-1980s and mid-1990s, appear to be driving the rental market. They are renting instead of buying for several reasons. Some have limited opportunities to finance the purchase of a home. Others want to remain mobile while pursuaing their careers. New construction is highest in cities like Austin, Washington, Chicago and New York, which are some of the prime designations for millenials.

While optimism is warranted, there are signs that the sector may have ignored the lessons of the 2008 recession. The availability of capital alone cannot be the determining factor driving development in a segment of the market that has become dominated by the addition of new supply. The real estate market must operate within the parameters of the greater economy, and that overall economy merits far less enthusiasm than the multifamily boom would suggest.

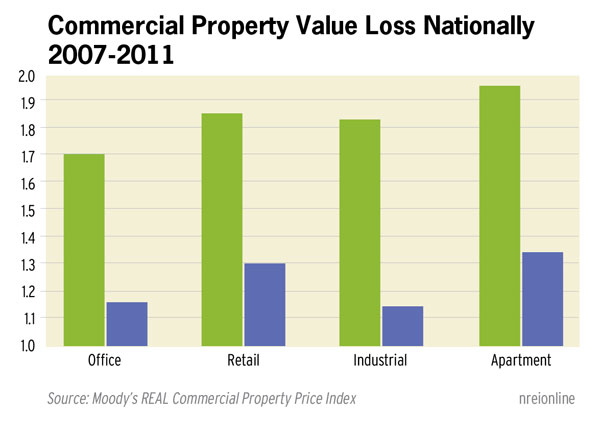

The liklihood of an over-supply in the apartment market raises interesting property tax concerns. The prospect of lower fundaments raises risk and lowers revenue expectations. Ultimately, it must be anticipated that pricing will change and values will decline.

Real estate taxes are based on market value, but the development of new values for real estate taxes lag well behind the market. In many places, the decline in value over the past five years still has not been fully recognized in the values established by assessors. Developers must have strategies in place which accelerate assessors' recognition of value changes taking place in the market. The key strategy to help owners keep real estate taxes in line with value changes is assiduous appeal of property tax assessments.

In 1989, the response to the savings and loan crises, the Uniform Standards of Professional Appraisal Practice were promulgated by the Appraisal Standards Board. These standards govern both the mass appraisal practices of assessors and the appraisal of individual properties by private appraisers, and will take into account the changes in the market as they arise. Thus apartment owners need to diligenty scrutinize their tax assessments in the next several years to ensure that these assessments reflect the changes in market values, and where they don't file an appeal.3