Understand the issues in filing strategic property tax appeals to reduce property tax.

Data centers are the current darling of CRE – which makes them a targeted sector of commercial real estate on which local assessors are laser focused. Due to the nature of the investment, there is less political heat for putting the tax burden on data centers. These taxpayers comprise a distant-faceless corporation, unlike other real estate classes who either have local employees or residents who can be affected by higher taxes. Combine the political ease with the fact that it is one of the few sectors that seems to have a clear growth forecast for the next several decades, ensuring that it's in for a tough battle with assessing offices. But the growth flurry in this marketplace shouldn't cause taxpayers to be unfairly taxed.

Data centers are a relatively new sector, compared to office, industrial and retail. The majority of assessors have likely had few, if any, of this property type in their townships. Thus, the probability that assessors have the understanding and expertise regarding the nuance and specialization of this property is highly unlikely, and a recipe for illegal taxation. It is critical that owners annually fight to keep their taxes at a reasonable level. A compelling argument, focusing on depreciation, business value and personal property allocation is critical.

Accelerated Depreciation

As Artificial Intelligence, AI, enters into its Golden Era, new requirements for data centers have exploded. The convergence of AI, autonomous driving vehicles, and smart residential properties will more than double the need for global storage capacity by 2027, according to JLL's Data Centers 2024 Global Outlook. But second generationcenters will have a difficult time getting their piece of the windfall.

AI clustered servers are much more powerful than previous servers and emit significantly more heat.Thus, the electrical and cooling requirements will be markedly different from the data center designs of the past. Energy efficient designs, locations in areas with affordable and reliable power supplies, sustainable power supplies, as well as local development incentives, will be the main drivers of demand moving forward.But as the new design requirements evolve in the future, the older centers will lose value quickly.

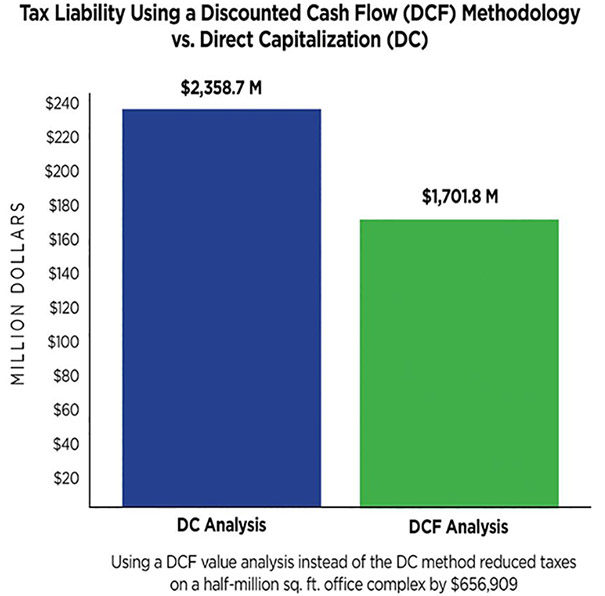

Depreciation is much more rampant on special use properties like data centers. Typically, an industrial building has as economic life of 50-60 years, with 2% annual depreciation. However, data centers will depreciate 5-10% annually. This is due to functional issues associated with the special use, according to Ed Kling, MAI Appraiser at Caton Valuation.

For example, the requirements of the mechanical and electrical hardware will be out of date within 15-20 years, according to Malcolm Howe, critical systems partner at engineering consultancy Cundall. Accelerating depreciation on 30% to 50% of the capitalized costs is typically achievable. Factors such as the level of security, the complexity of cooling systems, the number of redundant systems, and site improvements will determine this percentage.

Business Value

Assessors will wrongly assume that the rents associated with data centers, or their value in the market, is solely based on the bricks and stick of the real estate itself. However, as any operator is well aware, one can't disregard the business reputation of the owners and operators, as well. Much like hotels and self-storage, where the value differentials in many cases are due to the level of service, data center operators are known for their expertise. Users base their choice of vendors on criteria such as scalability (how can your needs grow with this provider), reliability (what is the historical uptime of the provider), deployment efficiency (can your infrastructure be set up timely and efficiently), network ecosystem (simplicity of multi-cloud interconnection and management) and financial stability (does the provider have a strong history or could it close within a year).

Unlike other commercial real estate, data center operators are actively monitoring every aspect of their properties to ensure that the client's data is secure. Generally speaking, if any building system fails in another real estate sector in the short term, the harm to the commercial tenant is minimal. However, short term system failure in data storage could mean the complete operations of an organization could be decimated permanently. Therefore, much like the energy costs to operate, the insurance costs are extremely high due to the multitude of risks inherent in providing services.

Similar to Hotels and Self Storage, data center owners are allowed to have a "return of" and a "return on" their personal property and operations investments, as well as deductions for management and reserves for replacement. Thus, some profits should be deducted with other expenses in calculating Net Operating Income.

But more importantly for the savvy operator, the appraiser should account for the stellar reputation of the operator compared to the general market. Logically, a provider with excellent business practices, highly functioning property management and historical success should be able to garner higher rents than other operators. But that escalated rent is due to the business of the operator, not the real estate itself.

Taxation as Personal Property

Data center operators also need to thoughtfully identify real property from personal property for taxation purposes. Forgoing this exercise may result in double taxation in states with personal property tax, or over taxation in states without personal property taxes where such property is wrongfully taxed by local assessors.

And the time is... now

Based on the strategies listed above, owners of data centers must thoughtfully appeal their assessed valuations on an annual basis. This sector must be looked at through a completely different lens than any other property type, due to the accelerated depreciation issues, strategic business value integrated into the property and potential for double taxation. Investors must work with seasoned professionals who understand the complexities of this product type and present the nuanced argument thoughtfully and convincingly to assessing official, or else the bottom line will be unfairly affected.