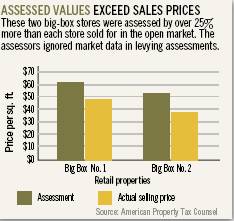

"Assessors prefer the cost approach because the availability of cost data from national valuation services makes the determination of a value rather straightforward.Taxpayers argue that an income approach is better suited to derive the value of a golf course..."

As the old joke goes, the fastest way to become a millionaire as a golf course owner is to start out with $5 million. Unfortunately some property tax assessors don't get the joke. They continue to assess golf courses as if their value is increasing or holding steady.

During the 1990s, the supply of golf courses expanded by 24% while the number of golfers rose by just 7%, according to the National Golf Foundation. What's more, in the first quarter of 2008 there has been a 3.5% drop in rounds played.

Golf course owners now face numerous challenges. Although more courses have closed than opened over the past two years, the oversupply will likely take several years to absorb. Additionally, the soft economy and rising oil prices negatively affect travel to golf courses and course operating costs.

Property assessors have failed to take these factors into account in making their assessments. But golf course owners have begun to fight city hall by filing property tax appeals. If successful, the appeals can result in significant tax savings.

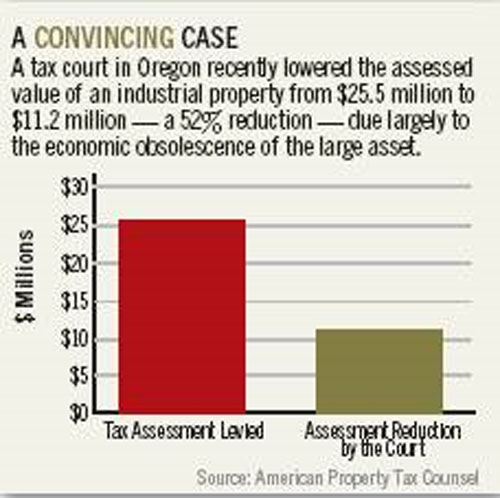

The accompanying chart demonstrates the magnitude of assessment reductions obtained by four different golf courses as a result of their tax appeals. On average, these appeals achieved a 40% reduction.

Why do assessors' valuations of golf courses differ so dramatically from the values contended by taxpayers and, in many instances, adopted by boards of equalization and judges? The assessor and taxpayer each use different valuation approaches that yield different values.

Methodology matters

The generally accepted valuation approaches include the cost, income capitalization, and sales comparison approaches. The appropriate valuation approach depends on various factors:

- the amount and reliability of the data collected in each approach;the inherent strengths and weaknesses of each approach as it relates to a particular property type;

- the relevance of each approach to the particular property at issue.

Assessors typically value golf courses using a cost approach. That approach starts with land value, adds the cost of property improvements, and subtracts physical depreciation. Assessors prefer the cost approach because the availability of cost data from national valuation services makes the determination of a value rather straightforward.

Assessors typically value golf courses using a cost approach. That approach starts with land value, adds the cost of property improvements, and subtracts physical depreciation. Assessors prefer the cost approach because the availability of cost data from national valuation services makes the determination of a value rather straightforward.

Taxpayers argue that an income approach is better suited to derive the value of a golf course. That approach starts with a determination of revenue and deducts operating expenses to arrive at net operating income. Net operating income is then divided by a capitalization rate, thus yielding the value.

The issue centers on which method of golf course valuation is preferable: the assessor's cost approach, or the taxpayer's income approach?

Courts side with owners

The judges in these cases rejected the assessor's cost approach for several reasons. The cost approach rests on the principle of substitution, but replacement sites are difficult to find in the golf course industry. One judge cited an appraisal industry publication, which concluded that the cost approach is generally inapplicable to golf courses.

The cost approach used by the assessor deducted only the physical depreciation, based on age, but did not factor in external obsolescence. External obsolescence results from outside forces such as the oversupply of courses.

Again, a judge cited the appraisal industry publication that noted the difficulty in estimating external obsolescence in a market where prices have fallen 50% or more since the late 1990s. The judges found that investors rarely use a cost approach to determine the purchase price to pay for a golf course.

The judges held that the income approach offers the best valuation method for a golf course because buyers typically buy courses to produce income. The approach measures this capacity and converts it into a projected sales price.

The assessor's cost approach has been found not to be par for the course, so owners should consult their property tax professional to determine if an income approach can reduce their property tax liability.

Not only are the rents affected by the first-generation tenant, the capitalization rate is significantly lower than market rates. The net-lease market into which these properties are sold is among the most active and developed in the real estate market, allowing for substantial liquidity, efficient pricing, and tax deferral through 1031 exchanges.

Not only are the rents affected by the first-generation tenant, the capitalization rate is significantly lower than market rates. The net-lease market into which these properties are sold is among the most active and developed in the real estate market, allowing for substantial liquidity, efficient pricing, and tax deferral through 1031 exchanges.

The business value reflects all the factors of production —— land, buildings, machinery and equipment, skilled labor, managerial expertise and goodwill. It is incumbent upon owners to show assessors how to separate the value of the real and personal property from the value of the business for assessment purposes.

The business value reflects all the factors of production —— land, buildings, machinery and equipment, skilled labor, managerial expertise and goodwill. It is incumbent upon owners to show assessors how to separate the value of the real and personal property from the value of the business for assessment purposes.