Introduction

This article provides an overview of real estate taxation in New York City (the “City”) including (i) the process by which the City assesses real property, (ii) how property owners challenge the City’s assessments, (iii) benefit programs available to reduce property owners’ real estate tax burdens, and (iv) the importance of understanding real estate taxes in lease negotiations. In New York City, real estate taxes have become an increasingly greater expense for property owners and landlords in recent years. As such, they are an ever-growing factor that any potential purchaser or tenant must account for in its business decisions. Counsel on either side of any real estate transaction should possess at least a basic knowledge of the real estate taxation process to be able to appropriately account for such taxes in negotiations. The process is complex, involves interaction with many government agencies, and is often counter-intuitive. Therefore, a working knowledge of the process is also important in order to understand that, for more complex transactions, specialized real estate tax representation might be necessary and appropriate.

New York City’s Department of Finance (DOF) is the agency charged with assessing all real property in New York City. DOF reassesses all real estate (over one million parcels) each year. Income generated from real estate taxes is the top source of revenue for the City, currently comprising over 40% of the City’s revenue. As a result, real estate taxes are a major factor to account for in the sale / purchase, and leasing of real estate. Furthermore, the City offers numerous real estate tax benefit programs that builders, developers, purchasers, landlords, and tenants need to be aware of in considering any transaction.

Procedures for assessing real property, challenging real estate tax assessments, and qualifying for the various tax benefit programs are governed by the New York State Real Property Tax Law (RPTL) and the New York City Charter, Administrative Code, and Rules.

Arriving at a Tax Assessment

Unlike most jurisdictions around the country, New York City reassesses every property on an annual basis and adheres to a strict and consistent calendar for publication of its assessment roll. Below is a summary of the key dates in the assessment process.

- Taxable Status Date. DOF assesses real property as of its status and condition each January 5, also known as the taxable status date. This date is particularly important when assessing properties that are experiencing large vacancies as of January 5 or are in various stages of construction and/or demolition. Since the status and condition of these types of properties are likely to change dramatically over the course of the year, their assessments the following year may experience similarly dramatic changes.

- Tentative vs. Final Assessment Dates. Each parcel of real property subject to assessment is identified on the New York City Tax Maps by a specific block and lot number. An individual tax lot may range from multiple buildings to just one residential or commercial unit in a condominium. On January 15, the City publishes tentative assessments for each tax lot. Between January 15 and May 24 the City has the authority to increase or decrease any assessment for any reason. This is called the change by notice period. During this time period taxpayers can also request a review of assessments if they feel such assessments were made due to usage of erroneous factors (i.e., incorrect square footage). Any changes to the tentative assessment made during this time must be sent to the taxpayer, in writing. The assessment roll closes on May 25 of each year, at which time the final assessment roll is published. This final assessment is the one upon which a taxpayer’s property tax bill is based and the one from which any challenge to the assessment will arise.

It is important for counsel to note that the tentative assessment published on January 15 is not the final word on a property’s tax burden. This assessment should be reviewed for potential errors that should be brought to the City’s attention in advance of the final roll’s publication on May 25. While the City sometimes adjusts errors on its own, there is an opportunity to alert them to potential issues. It is also important to note that this change by notice period exists separately and apart from the administrative and legal challenges to an assessment that take place later and have different deadlines associated with them. That process is discussed in greater detail below.

The Property Tax Bill

When the tentative assessment roll is released each January, DOF provides taxpayers with a notice of value. The notice of value includes many numbers and terms which may cause confusion, but which are important to understand for purposes of what a taxpayer’s real estate tax obligation will ultimately be based upon. Below is a summary of the key terms to understand in the notice of value.

Equalization Rate: In assessing properties, DOF first derives a parcel’s market value which is the City’s determination as to what the property is worth. The City, other than the few exceptions discussed below, assesses properties at 45% of their market value. This is the City’s equalization rate.

Actual Assessment: The City applies the 45% equalization rate to a property’s market value to arrive at its actual assessment.

Transitional Assessment: To shield taxpayers from sudden and drastic annual fluctuations in assessed value, the City provides for a five-year “phase-in” of every property’s actual assessment. Other than an important exception discussed below, this number is generally an arithmetic average of the five most recent years’ actual assessments and is known as the transitional assessment for a property. A property’s real estate tax liability is based on the lower of the actual vs. transitional assessment. As a result, if a property’s actual assessed value increased by $1 million over the previous year’s assessment, the transitional assessment would really only be incorporating 20% of that increase into this year’s transitional assessment. The taxpayer will not bear the full brunt of that large increase immediately.

As an example, take a hypothetical apartment building in Manhattan with the following values and assessments:

Tax Year | Market Value | Actual Assessment | Transitional Assessment |

17/18 | $8,100,000 | $3,645,000 | $2,587,500 |

16/17 | $6,400,000 | $2,880,000 | $2,173,500 |

15/16 | $5,500,000 | $2,475,000 | |

14/15 | $4,750,000 | $2,137,500 | |

13/14 | $4,000,000 | $1,800,000 | |

12/13 | $3,500,000 | $1,575,000 | |

As you can see, the actual assessment increased by almost $1 million from $2.88 million in tax year 16/17 to $3.645 million in tax year 17/18. However, because the transitional assessment incorporates the five most recent actual assessments, the transitional assessment only increased by about $400,000. The real estate taxes for the property will therefore be based on this lower ($2,587,500) amount. Note that tax years 12/13 – 15/16 would also have transitional assessments based on actual assessment of years not listed. For purposes of illustration only, the focus of this chart is on the two most recent tax years (15/16 and 16/17).

An important exception to note regarding transitional assessment phase-ins comes up when there is construction or demolition being done on a property. In those instances the City adds or subtracts what is called a “physical increase” or “physical decrease” to the property based on the value added or subtracted for the construction or demolition taking place. This physical increase or decrease is not subject to a five-year transitional phase-in and is taxable in the year in which it took place.

Tax Rate: After determining the appropriate billable assessment, a tax rate is applied to the billable assessed value to come up with the real estate tax liability for a particular property. The tax rates vary depending on the class of property being assessed (see below). The rates are set annually by the New York City Council and are not subject to challenge.

Assessment of Different Classes of Property

Real property in New York City is divided into four classes, each with distinct assessment rules as detailed below:

- Class 1. Properties in tax class 1 consist of primarily residential properties with three or fewer residential units. Essentially these are one, two, and three family homes. Properties in class 1 enjoy highly favorable treatment from a real estate tax perspective. As discussed above, while the City assesses the vast majority of properties at 45% of their city-determined market values, properties in class 1 are assessed at only 6% of their market values. This generally makes their assessed value (and as a result, their real estate tax bill) much lower as compared to the other classes of property. Furthermore, state law places caps on the amount the assessed value for class 1 properties is permitted to increase each year. Specifically, properties in tax class 1 cannot see their assessment increase by more than 6% year over year and by more than 20% over any five year period. As with all other properties, any physical changes to the property are not subject to these statutory limitations on increases and can result in increases that are larger than 6%.

- Class 2. Properties in class 2 are primarily residential properties with more than three units. Class 2 includes residential apartment buildings as well as cooperatives and condominiums. Within class 2 is a subset of properties (class 2a, 2b, and 2c) that enjoy limitations on assessment increases similar to those that properties in tax class 1 enjoy. Specifically, primarily residential properties in class 2 with fewer than 11 units cannot see their assessments increase by more than 8% per year and by more than 30% over any five year period. These properties include rental properties as well as cooperatives and condominiums. Class 2a properties contain 4-6 residential units; class 2b properties contain 7-10 residential units; class 2c properties are cooperative or condominium properties with 3-10 units. While they are still assessed at 45% of market value (as opposed to the 6% equalization rate for class 1), the statutory caps still provide a benefit to these smaller residential properties. Transitional assessments do not apply to this subclass.

Many of these smaller residential properties that may qualify for favorable tax treatment by being within class 2a, 2b, or 2c also contain a commercial component. Since commercial properties fall within tax class 4 (see below) and do not enjoy any statutory limitations on increase, it is important for an owner hoping to qualify for these statutory caps to make sure the property is considered primarily residential. There is no explicit definition of primarily residential and, over the years, the City has had various policies in determining whether something should be considered primarily residential or commercial. Previously, the City looked at which component generated greater rental income for the building and considered that to be its “primary” function. More recently, greater weight seems to be given to overall commercial vs. residential square footage as well as to the total number of commercial versus residential units within the building in determining whether it would be considered primarily residential for purposes of receiving class 2a, 2b or 2c status.

On April 25, 2017 a coalition seeking tax reform called Tax Equity Now filed suit against New York City and New York State in New York State Supreme Court seeking a declaratory judgment that the entire New York City real property tax system is unconstitutional on various grounds. Specifically, the lawsuit targets the inequity and alleged constitutional infirmities created by the beneficial treatment of class 1 properties and smaller class 2 properties (described above) at the expense of other real estate tax payers among the other tax classes. Furthermore, the suit goes on to claim that this unequal treatment among the tax classes has a disparate impact on minorities. Tax Equity Now claims that since minorities in the City are predominantly tenants in larger class 2 rental apartment buildings which are not subject to any favorable tax treatment, minorities pay a disproportionate share of the City’s tax burden. As a result, wealthier, predominantly non-minority homeowners pay a disproportionately lower real estate tax burden. While this lawsuit will likely take years to be resolved and is not of immediate concern to the accuracy of the information in this practice note, it something to be mindful of as it works its way through the courts.

- Class 3. Properties in tax class 3 consist primarily of utility properties (i.e., power plants). These are also assessed at 45% of market value.

- Class 4. Class 4 is all properties that do not fall within tax class 1, 2, or 3. These are essentially all commercial properties, including office buildings, retail spaces, hotels, parking garages, etc. Under New York State law, certain utility related equipment is also considered real property for the purposes of assessment and falls into tax class 4. This property is known as Real Estate Utility Company (REUC) property and is separately assessed by the City of New York. The most common type of property that is assessed as REUC property is emergency backup generators. The assessment of these generators has become increasingly important in the wake of Super Storm Sandy as the sheer number of generators in the City has increased exponentially. From an assessment policy perspective, the City actually differentiates between tenant-owned and building-owned generators. Specifically, generators that are owned by the building are not separately assessed, as they are considered part of the building and, therefore, their presence is deemed to have already been incorporated into the building’s assessment. Conversely, tenant-owned generators are separately assessed and given their own unique REUC Identification Number, which is basically the equivalent of an individual tax lot for assessment purposes. These generators are considered more portable, are more likely to travel with the tenant, and are, therefore, not reflected in the overall assessment of a building.

Particularly with respect to REUC properties, counsel should understand and be aware of the intentions of both sides with respect to backup generator equipment. Do tenants plan to install their own backup generating systems? Will they use some other backup system already in place in the building? These backup generators are not traditionally the type of item one would consider “real estate,” however, New York State Law defines them as such. Furthermore, City policies treat these generators differently based on their ownership status. As a result, they may be subject to additional real estate taxes not initially contemplated in any deal.

Three Methods of Real Property Valuation

Set forth below are the three methods of valuation typically used in assessing real property.

- Income Capitalization Approach. The City assesses the vast majority of properties using the income capitalization approach. By law, most owners of income-producing properties are required to provide annual real property income and expense statements to the City (referred to as RPIE). In the simplest cases, the City reviews and adjusts these numbers to arrive at a net operating income for the property. It then applies a capitalization rate to the property to arrive at a market value for the property. As discussed above, the City then generally takes 45% of that market value to arrive at an assessment. However, strictly and blindly applying RPIE numbers to arrive at an assessment becomes difficult when issues of vacancies, construction, and other factors result in the RPIE numbers not necessarily being a reflection of a property’s true value. In these cases, DOF will generally make various adjustments to a property’s net operating income based on annual guidelines and parameters DOF establishes for the various types of properties it is responsible for assessing.

Obviously residential co-ops and condos do not report rental income. Therefore, in order to arrive at a net operating income (and ultimate assessment) for these properties, New York State law requires that co-ops and condos are to be valued and assessed as if they were rental properties. This results in City assessors looking to the rental income market of what they deem to be comparable buildings and applying those rents to the co-ops and condos to arrive at their assessments. A successful challenge to the assessment of a residential co-op or condo would require finding other comparable rentals that more closely reflect and mirror the situations at the subject property being assessed. Since commercial condominium units typically do pay rent, the City assesses them as they would any other individual block and lot. The one caveat is that, since an individual commercial condominium unit is usually part of a larger building containing many condominium units, DOF will generally assess a specific unit based on its percent interest in the common elements of the building as a whole. This percentage figure is listed in the condominium’s declaration. As a result of this methodology, the percent interest of a particular condominium unit is an important factor in the unit’s ultimate tax bill and the ultimate allocation should be considered carefully when drafting and reviewing the condominium offering plan.

- Cost Approach. City assessors primarily use the cost approach in valuing specialty properties or equipment (power plants, generators, etc.). They arrive at the assessment by determining what the current cost would be to build a new identical specialty property and then deduct from such cost for depreciation.

- Sales Approach. The City has a policy to not reassess properties based on sales prices. Property sales may be used as evidence of value when challenging a property’s assessment; however, they are not the basis of an assessment. The City does review sales when valuing class 1 properties (1, 2, and 3-family homes) and to arrive at market values for those properties. However, as discussed above, since the permissible annual assessment increases for class 1 properties are capped, the market value the City applies based on comparable sales generally has no bearing on the assessment.

How to Challenge an Assessment

As discussed above, DOF publishes tentative assessments for all properties on January 15 of each year. A property owner (or other party with standing) who wishes to challenge that assessment must do so by filing an application with the New York City Tax Commission (the Tax Commission) by March 1 (note that for class 1 the deadline is March 15). Most properties also require the filing of an income and expense statement, which must be filed by March 24. Failure to timely meet these deadlines is a jurisdictional defect which precludes an owner from challenging that year’s assessment.

In order to challenge an assessment, a party must have standing to do so. Generally, any party claiming to be aggrieved by an assessment has the right to challenge that assessment. This has been defined as anyone whose pecuniary interest may be affected by an assessment. As a result, not just property owners, but tenants, partial tenants, and other parties responsible for the payment of real estate taxes may have standing to challenge the assessment upon which those taxes are based.

The Tax Commission is the administrative agency charged with reviewing the assessments issued by DOF. It schedules hearings to review the assessments of all properties that file timely challenges each year. These hearings are held from late spring to early fall each year. At the hearings, the Tax Commission generally reviews the two most recent years’ assessments. However, legally, the agency has jurisdiction to review any two of the five most recent assessments. The Tax Commission may decide to offer a reduction in an assessment or confirm DOF’s assessment. The Tax Commission is prohibited from raising a property tax assessment as a result of a hearing.

DOF publishes its final assessment roll on May 25 of each year.

By June 1 of each year property owners are required to file income and expense statements with DOF, reporting their numbers from the prior calendar year. This is the RPIE filing (discussed above), which must be completed online through DOF’s website.

If an owner is unable to resolve its assessment challenge with the Tax Commission in a particular year, the owner must file a petition in New York State Supreme Court by October 24 of each year in order to preserve its right to litigate over the assessment.

Grounds for Court Challenges/Trials

If an assessment challenge proceeds to trial there are four grounds under which that assessment may be challenged. The assessment must be alleged to be: (i) excessive, (ii) illegal, (iii) unequal, or (iv) misclassified. The vast majority of trials involve a claim of overvaluation.

Trials over an assessment are generally bench trials. The City agency responsible for handling assessment-related litigation is the New York City Law Department. At trial, generally, each side submits an expert appraisal report with conclusions of value and the expert real estate appraiser who prepared the report testifies at the trial. Testimony is usually limited to the four corners of the report.

City assessments are deemed presumptively valid so the burden is on the petitioner to show the assessment was incorrect. Much as in the case of administrative review of the assessment at the Tax Commission, a court is prohibited from raising an assessment as the result of a trial. The City’s assessment can only be confirmed or reduced at trial.

Recently, DOF has provided an additional administrative avenue to challenge an assessment on the grounds that it was based on a clerical error or error of description. New York State law has had a longstanding procedure by which to challenge assessments based on clerical error, however, those sections of the RPTL were inapplicable to New York City. As a result, the City recently amended its rules to codify and apply similar procedures. The types of errors DOF considers under these rules include, but are not limited to, errors in assessments due to: computation errors, incorrect square footage, incorrect number of units, incorrect building class, as well as all other clerical errors specified in Article 5 of the RPTL. DOF will specifically not consider clerical error challenges if the challenges have to do with valuation methodology, incorrect comparables and other valuation-related challenges that are more appropriately challenged in the standard ways described above. Much like New York State law, the new City rules allow DOF to look back up to six years prior to the time a clerical error challenge was filed when considering changing an assessment on these grounds.

Benefit, Abatement, and Exemption Programs

The City offers a wide variety of real estate tax exemption/abatement programs to encourage development of new buildings and renovation of existing buildings, among other things. Below is a summary of the most commonly utilized programs.

- Industrial Commercial Abatement Program (ICAP). ICAP provides tax abatements for renovating commercial buildings and, in some parts of the City, for building brand new industrial/commercial buildings. In some instances even renovated or newly built retail space can qualify for ICAP benefits. Abatements can last as long as 25 years in some cases and protect a developer from the large increases in value (and consequently, real estate tax assessments) that normally results from these large development projects. There are complex filing procedures and requirements to be met and maintained during the duration of the project in order to qualify for the benefit, including minimum required expenditure amounts and requirements for soliciting Minority and Women-Owned Businesses (MWBE) for the work being done.

- 420 Benefits. This program provides various tax abatements/exemptions for properties owned by charitable and not-for-profit entities. There are initial requirements that must be met and substantiated in order to qualify as well as certification of continuing charitable or non-profit use in order to ensure the benefits remain in place each year.

- J-51Program. This program provides a property tax exemption and abatement for renovating and upgrading residential apartment buildings. The benefit varies depending on the building’s location and the type of improvements.

- 421-a Program. In April, 2017 legislation was signed amending and replacing the previous 421-a program to create the new Affordable New York Housing Program. This program applies to new construction of multi¬family residential buildings and eligible conversions and provides eligible projects with substantial tax savings, in some cases up to 35 years of real estate tax abatements (in addition to a three year abatement during construction). To benefit from the tax savings, some significant requirements must be met - for example, all projects must be comprised of at least 25% affordable units. For projects located in specific areas and comprised of more than 300 units, certain wage requirements for construction workers also apply. The program applies to both rental and condominium/co-op projects though the eligibility for condo/co-op projects has more restrictions. (3) This new version of the 421-a program applies to eligible projects that commence between January 1, 2016 and June 15, 2022. As of May, 2017, the law is brand new and there are nuances that will likely need to be resolved by the City in its rule making process, however, the key point is that this benefit for new residential projects will once again be available to developers.

- Exemptions for Individual Homeowners. Many individual home and apartment unit owners may qualify for certain property tax reductions pursuant to programs such as the cooperative/condominium abatement, School Tax Relief Program (STAR), Senior Citizen Exemption, Disabled Homeowners Exemption, Veterans Exemption, and Clergy Exemption. Applications for benefits must be made annually as changes in circumstances (i.e., transfers) each year may take a unit out of eligibility for the various programs.

- Progress Assessments. While not part of any formal exemption or abatement program, New York City law does allow for some tax relief for the construction of new commercial and residential buildings. It is a general rule of assessment in the City that a building in the course of construction, commenced since the preceding fifth day of January and not ready for occupancy on the fifth day of January following, shall not be assessed unless it shall be ready for occupancy or a part thereof shall be occupied prior to the fifteenth day of April. All newly constructed commercial and residential buildings are entitled to at least one year of this so-called “progress assessment” whereby any building assessment placed on the property would be removed. With the exception of hotels, new commercial buildings can actually get up three years of progress assessments while in the course of construction if the building is not ready for occupancy each April 15. This essentially allows for up to three years of no building assessments while in the course of construction.

The programs noted above are important for counsel to be aware of. When representing an owner, any discussion regarding major construction projects and changes to a building should be considered in the context of potential availability of some of these benefit programs. They can play a huge role in reducing an owner’s tax burden and making contemplated projects more economically feasible. Similarly, counsel representing a purchaser should be aware of any plans the purchaser may have as far as construction and/or converting the nature of the building (i.e., from commercial to residential) as these types of changes have substantial property tax ramifications as well as potentially substantial benefit programs that may help mitigate potential increased liability.

Tax Certiorari Lease Provisions/Exemption Lease ICAP Provisions

Real estate taxes in New York City are becoming an increasingly large portion of landlords’ and tenants’ investment calculations and it is vital to account for real estate tax issues in commercial leasing. Determining whether a landlord or a tenant is responsible for payment of the taxes and who has the right to challenge the taxes is just one issue. Tax escalation clauses and how payments are spread among the tenant and the landlord, as well as choosing an appropriate base year from which said real estate tax escalations begin, are essential components to any commercial leasing negotiation and often make or break deals.

Knowledge of assessment procedures and DOF calendars for when rental figures will be used in assessments is vital in determining base year real estate tax payments and how increases in tax payments are to be determined on a going-forward basis. These issues must also be accounted for in commercial leases. Finally, provisions regarding which party benefits from any abatement programs (if applicable) need to be negotiated in any lease.

This will certainly affect overall rental and tax payments. Many negotiated real estate transactions hinge on real estate tax projections going forward. Projecting future real estate taxes is fraught with uncertainty. However, with comprehensive knowledge of how the system works, one can make reasonable estimates. It is these estimates and projections that are frequently the basis for lease negotiations. Specialized real estate tax counsel may be retained to assist in these projections and to review drafts of leasing documents.

Conclusion

At the very least, when entering into a real estate transaction involving property in New York City, counsel should be aware of New York City’s complex real property tax process and how the issues surrounding that process may affect his or her clients. The process of challenging property taxes involves a complicated assessment procedure system on the part of the City as well as multiple required filings throughout the course of the year, which must be complied with in order to even have the opportunity to challenge one’s assessment.

An understanding of the assessment process, how real estate taxes are calculated, and the benefit programs the City makes available to property owners will allow counsel to better negotiate on behalf of clients. Failure to accurately and meticulously account for the increasingly important role that real estate taxes play will put counsel at a major disadvantage.

Steven Tishco is an associate at Marcus & Pollack, LLP. Mr. Tishco concentrates his practice on real estate tax assessment and exemption matters (tax certiorari). He handles all types of real estate tax disputes and appears regularly before the Courts of the State of New York and various New York City agencies. His experience includes litigation and trial work involving the valuation of residential and commercial properties. The law firm of Marcus & Pollack LLP, is the New York City member of American Property Tax Counsel (APTC), the national affiliation of property tax attorneys. He can be reached at stishco@marcuspollack.com

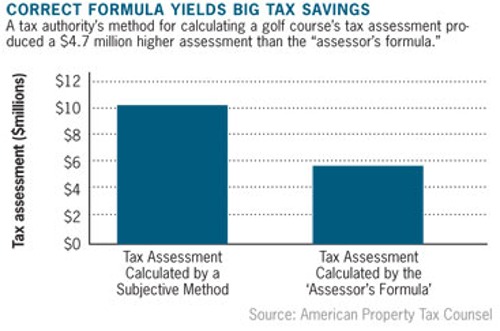

A red flag

A red flag

One prominent Long Island club recently sold to a developer. Another declared bankruptcy, and surviving golf courses are fighting to avoid similar fates. Closures outpace new openings as demand for golf declines and revenue growth remains flat in the face of rising costs especially property taxes.

One prominent Long Island club recently sold to a developer. Another declared bankruptcy, and surviving golf courses are fighting to avoid similar fates. Closures outpace new openings as demand for golf declines and revenue growth remains flat in the face of rising costs especially property taxes.