"Property owners haunted by flawed approach to tax assessments..."

Flawed cost-based assessments are a common cause of unlawfully high property taxation. Year after year, inflated valuations by government assessors can impose excessive tax bills on a property, notwithstanding annual taxpayer efforts to correct them.

For property owners, persistently unfair assessments are like Talky Tina, the infamous talking doll in the television series The Twilight Zone. The evil toy ultimately prevails against homeowner Erich Streator, notwithstanding his repeated efforts to remove the doll from the Streator family home. The bad news for taxpayers is that assessors will continue to impose excessive, flawed assessments because they often employ error-prone appraisal methods in the interest of expediency. The following demonstrates a common route to a cost-based assessment.

Software can help assessors quickly calculate the cost of reproducing property improvements, an amount I'll call "cost to build today." To account for physical deterioration of improvements, assessors can use an age-life method.

For example, let's say a five-year old structure's estimated life is 50 years and its cost to build today is $10 million. The assessor deducts 10% for physical deterioration and adds the resulting $9 million value to the land value for a quick — and often inflated — assessment. The good news for taxpayers is that, unlike the Twilight Zone's Streator family, they have the means to seek and obtain justice.

A compelling case

A recently litigated tax appeal regarding a big-box retail building offers a persuasive example. The taxpayer-submitted appraisal included not only income- and sales-comparison based valuations, but also a proper cost approach.

The cost-based analysis differed in several ways from the tax assessor's hasty valuation. First, the appraisal explained that in addition to physical deterioration, depreciation must reflect functional obsolescence or drawbacks to the property itself, as well as external obsolescence. The latter refers to factors outside the property, such as reduced demand for space due to a recession.

The taxpayer proved that the original assessment was flawed because only physical deterioration had been subtracted from the cost to build today. Additionally, the property owner's appraiser presented comparable sales of other big-box locations where a taxpayer had purchased a site, developed a building and sold the property within a few years. These comparable sales were properties in which the owners had a fee simple interest.

For each comparable sale, the appraiser established the total depreciation of the improvements by first subtracting the original land purchase amount from the recent sale price to arrive at a current depreciated value for the building. Then the appraiser compared that building value to the cost to build today, which showed how much the building had depreciated over time.

The total depreciation at these similar properties supported the case for a lower assessment. In the most extreme example from several comparable sales, the value of the building and improvements was 56% less than the cost to build today. Total depreciation of the improvements in the comparable examples ranged from 42% to 56%. Applying this analysis, even after adding back the property's $700,000 land cost, the property assessment should have been about $3 million instead of more than $5 million.

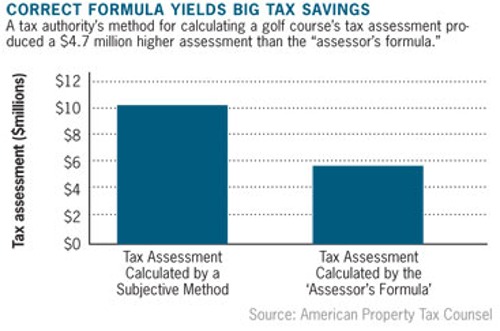

In this case, the appraiser had comparable sales data on similar properties where land acquisition, construction and a sale had taken place in a relatively short time. In cases where the available comparable sales are of older properties, land sales may be used to establish the land value, rather than using the actual original price. As the accompanying chart shows, the taxpayer demonstrated that the government's assessment was unlawfully inflated by over 40%. Clearly, comparable sales can help taxpayers fight the kind of excessive taxation that should only exist in the fictitious world of The Twilight Zone.

One prominent Long Island club recently sold to a developer. Another declared bankruptcy, and surviving golf courses are fighting to avoid similar fates. Closures outpace new openings as demand for golf declines and revenue growth remains flat in the face of rising costs especially property taxes.

One prominent Long Island club recently sold to a developer. Another declared bankruptcy, and surviving golf courses are fighting to avoid similar fates. Closures outpace new openings as demand for golf declines and revenue growth remains flat in the face of rising costs especially property taxes.

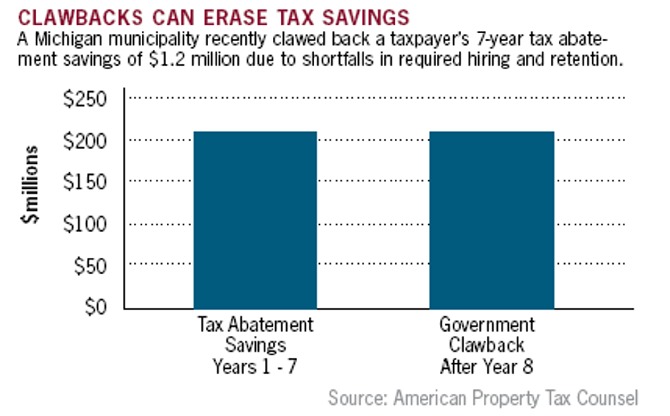

In some situations, a taxpayer should consider renegotiating the abatement agreement. A business can be in a surprisingly strong negotiating position, especially in instances where it can boast contributions to the local economy.

In some situations, a taxpayer should consider renegotiating the abatement agreement. A business can be in a surprisingly strong negotiating position, especially in instances where it can boast contributions to the local economy.

Prediction of a property's ability to generate income is precisely what the income approach to value in property assessment attempts to accomplish. The income approach estimates future benefits from ownership of the property. But this estimate requires extensive market research to evaluate risk factors in order to accurately predict income streams and expenses.

Prediction of a property's ability to generate income is precisely what the income approach to value in property assessment attempts to accomplish. The income approach estimates future benefits from ownership of the property. But this estimate requires extensive market research to evaluate risk factors in order to accurately predict income streams and expenses.

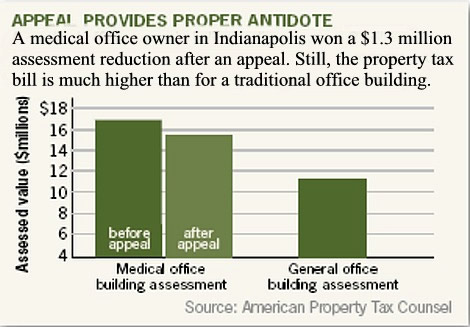

As a result of this painstaking development and presentation of the relevant facts, the Appeal Board ruled in favor of the taxpayer and reduced the property's valuation by $1.3 million to $15.6 million. While this reduction was warranted, the medical office building remains valued higher than the general office building, proving that medical office buildings pay higher property taxes.

As a result of this painstaking development and presentation of the relevant facts, the Appeal Board ruled in favor of the taxpayer and reduced the property's valuation by $1.3 million to $15.6 million. While this reduction was warranted, the medical office building remains valued higher than the general office building, proving that medical office buildings pay higher property taxes. An owner or property manager examining the rental income from the office property above can rest easy because it's clear that no problem exists. Here's a well-managed property fully leased in a weak economy. However, taxpayers must not be lulled into ignoring the need for a review of any tax assessment received in an economy under duress.

An owner or property manager examining the rental income from the office property above can rest easy because it's clear that no problem exists. Here's a well-managed property fully leased in a weak economy. However, taxpayers must not be lulled into ignoring the need for a review of any tax assessment received in an economy under duress.